This article is from our content partner, CorpHedge

This year has been exceptionally marked by the weakness of the U.S. dollar. In the first half of this year, the trade-weighted U.S. dollar declined by more than 8%, marking the greenback’s worst mid-year performance in over 40 years. For me, this is a stark reminder that currencies can experience incredibly sharp trends. As long as we see range-bound markets, it’s easy to feel secure in a static hedging policy. But when a significant move occurs, it forces us to ask the tough questions: Is our policy good enough? Where can we improve?

In my experience, CFOs and treasury professionals often fall into two camps: those who strictly adhere to a pre-defined policy regardless of market conditions, and those who take a more opportunistic, yet still risk-averse, approach. I’d like to analyze how we can build a better, more dynamic hedging policy. The starting point for any company must be a clear-eyed assessment of its own risk appetite.

From there, we need to consider both internal and external factors. The internal, subjective factors include the company’s risk tolerance and the time pressure of its forecasted flows. For instance, a near-term payment for an acquisition carries immense time pressure, whereas a more speculative, long-term forecast has less urgency.

Next, we must analyze the external market factors. When executing derivative transactions, we are dealing with financial markets shaped by a multitude of signals. For those of us aiming to hedge effectively, I believe a few are particularly critical to watch:

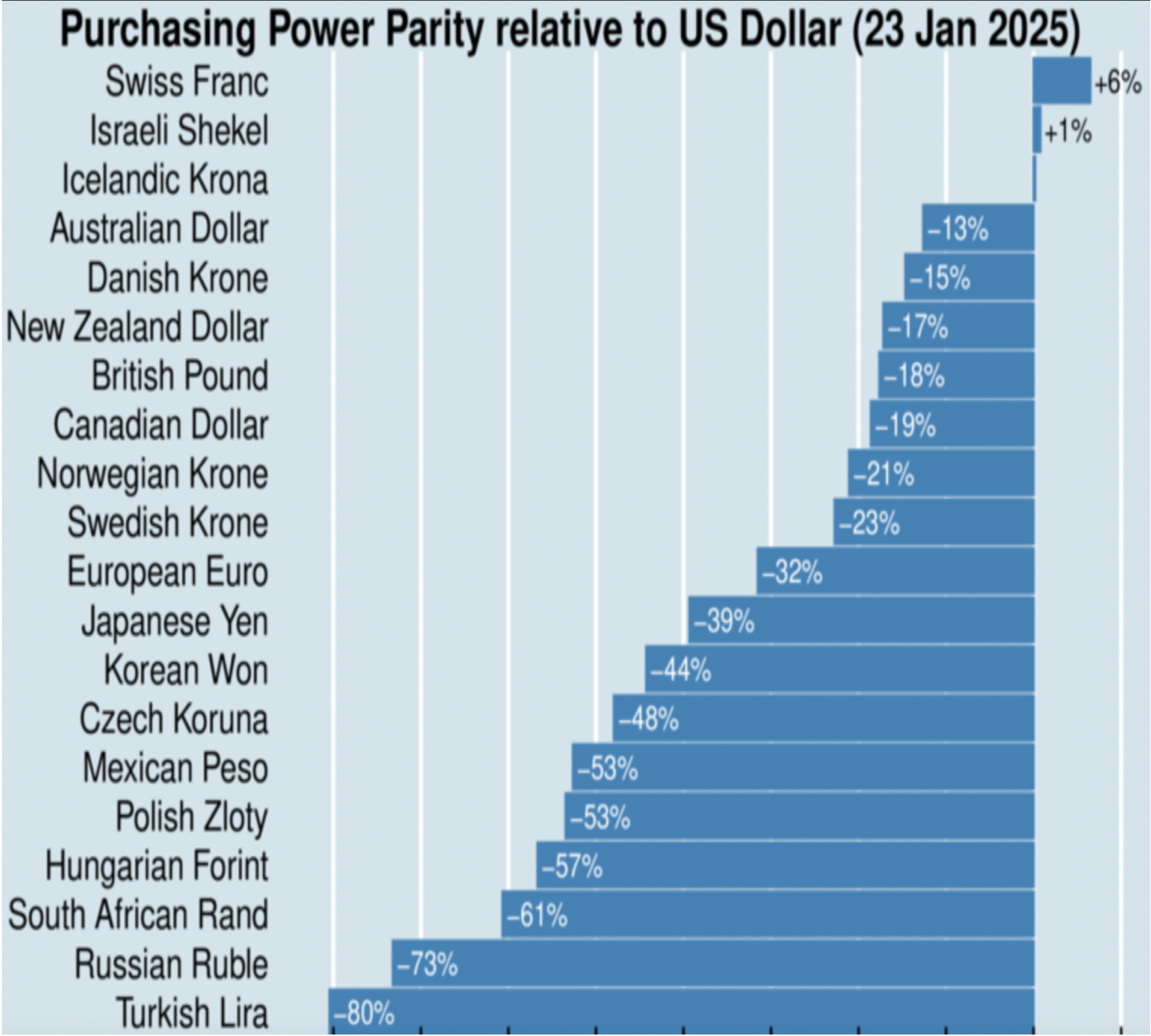

1. Valuation: What is the currency’s current value compared to its Purchasing Power Parity (PPP) level? While currencies are expected to revert to their PPP fair value over time, this correction can be very slow. A more useful concept for treasurers is the ‘half-life’ of the deviation. According to research by Craig (2005), this is the time it takes for half of the over- or undervaluation to disappear. His findings show that for major currencies far from their fair value, this process often takes about 12 to 18 months, giving us a more practical timeframe than just “the long run.”

2. Volatility: As risk managers, volatility is crucial. We should ask not only how current implied or realized volatility compares to historical levels, but also: What is the current volatility percentile? Is it unusually high or low? This context is key.

3. Interest Rate Differentials (Carry): This factor directly determines hedging costs, but its analysis requires nuance. From a classic Wall Street perspective, the carry trade involves borrowing in low-yielding currencies (like the JPY or, until recently, the USD) to buy higher-yielding ones (like the AUD or NZD).

However, the recent environment has been unusual. The U.S. dollar, typically a funding currency, has acted more like a high-yielding one compared to the euro or yen. This created a powerful incentive for companies to leave their USD-denominated inflows unhedged, hoping to profit from the high yields and the belief that the dollar would only get stronger.

But this strategy has a well-known vulnerability. During major risk-off events, like the 2008 financial crisis, these carry trades can unwind violently, leading to massive losses. This is why, as a risk manager, I argue against looking at interest rate differentials in isolation. A much more powerful metric is the risk-adjusted carry.

This means we don’t just look at the yield pickup; we adjust it for the currency’s volatility. This leads us to the carry-to-risk ratio, often calculated by dividing the interest rate differential by 30-day volatility. A higher ratio suggests a more favorable risk-reward profile, while a lower ratio signals potential danger in a risk-off scenario. In my view, this is a far superior tool for cross-currency analysis.

The Recent USD Story: A Perfect Storm

At the beginning of this year, the USD was overvalued by about 32% according to PPP data. The context was a U.S. administration keen on reducing the trade deficit, implying a desire for a cheaper dollar. With this uncertainty, it was no surprise that volatility rose significantly. The currency was overvalued, and volatility was rising sharply—a classic recipe for a major downward move.

PPP data at the beginning of the year (OECD):

A recent paper from the Bank for International Settlements (BIS) confirmed what happened next: the dollar’s decline was accelerated by a rush to hedge. For a long time, the consensus view of USD strength, combined with low volatility and high hedging costs, meant many flows went unhedged. The BIS noted that Japanese life insurance companies, for example, had only hedged about 40% of their flows from 2021-2024. When they and others rushed to increase hedges in April, it triggered aggressive dollar sell-offs, creating a chain reaction that fueled the aggressive downward trend we witnessed.

How to Build a Better Hedging Policy

I believe that in this day and age, with data so accessible and technology so advanced, applying the same static hedging principles from 20 years ago is a mistake. We can and should be more sophisticated.

This sophisticated approach involves building a framework that assigns weights to the key factors: fair value (PPP), volatility, and risk-adjusted carry. This model should also incorporate your company’s internal factors, like risk aversion and the time pressure of its cash flows.

All of this can be consolidated into a scoring system. The output is a dynamic optimal hedge ratio that moves based on changing conditions. Instead of being fixed, your hedge percentage might increase or decrease from the static baseline required by your layering policy. This approach makes your policy more intelligent and precisely aligned with both market conditions and your company’s risk profile.

Under such a system, high-quality, up-to-date data becomes paramount. By adopting such a dynamic method, a company can significantly enhance its hedging policy, allowing it to stay closer to the market while ensuring it remains protected from adverse financial impacts.

Join our Treasury Community

Treasury Mastermind is a community of professionals working in treasury management or those interested in learning more about various topics related to treasury management, including cash management, foreign exchange management, and payments. To register and connect with Treasury professionals, click [HERE] or fill out the form below to get more information.