Treasury for Non-Treasurers (3rd article, part 5)

“All happy families are alike; each unhappy family is unhappy in its own way.”

This quote from Tolstoy’s Anna Karenina is apt for tactical treasuries. Personnel who have worked only in strategic and operational treasuries don’t know things could be different. They are “happy.

”Those in tactical treasuries, on the other hand, know they can be different and better. Each is, if not “unhappy,” at least dissatisfied.

In this article, we’ll review tactical treasuries and, later, introduce the idea of “The Chasm.”

A quick recap on strategic and operational treasuries

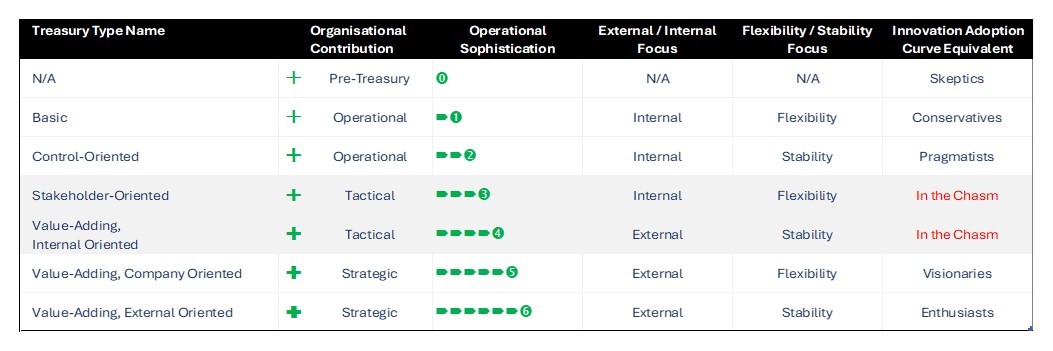

You won’t be surprised to hear that there are two types of tactical treasuries: Stakeholder-Oriented and Value-Adding Internal-Oriented ones. We’ll review each in turn and discuss their impact on business performance. First, let’s quickly recap the types of treasuries we’ve discussed in previous articles:

- Basic treasuries usually have one employee, typically located at head office. They manage the financial operations of the head office and get involved with other functions only when the CFO requires it. These are operational, internal, and flexibility-focused.

- Control-oriented treasuries, on the other hand, are designed to reduce financial risks. Policies, systems, additional staff, procedures, and reporting remove as much flexibility as possible, not just for central treasury but also for the whole organization. They are stability-focused but still perform basic financial transactions, just on a larger scale.

In the second part of this third article, “A Tale of Two Operational Treasuries,” I shared my experience of building a control-oriented treasury from a basic one.

- At the other end of the spectrum, value-adding external-oriented treasuries like IATA Financial Services and Ford Motor Credit are separate financial lines of business. They value predictable results, have substantial human and capital resources, and operate with autonomy.

- Value-adding company-oriented treasuries are similar to external-oriented treasuries, as they are profit centres. However, they are not self-contained businesses; they are support functions that provide flexible financial services to other departments, helping them interact more effectively with the company’s stakeholders. For instance, IBM’s European Treasury Centre, which I worked in, supported the European subsidiaries’ computer purchase financing functions by providing them with funding and taking over all associated financial risks.

Tactical Treasuries

You can see a pattern here. The treasuries we’ve discussed have internal vs. external and flexibility vs. stability focuses. We’ve covered the four possibilities. So, what are tactical treasuries, then?

Let’s revisit the image in article 2, “Is Treasury a Strategic Function,” and expand the previous table.

Tactical treasuries are those who sit between pragmatists and visionaries. As you can imagine, its a huge gap. This is the chasm we’ll talk about in the next articles: How it happens and how to cross it.

Stakeholder-Oriented Treasuries

Stakeholder-Oriented Treasuries are like internally-focused, Control-Oriented Treasuries but they have specialists within them who are externally-focused.

Stakeholder-Oriented Treasuries are like Control-Oriented Treasuries: they are internally- and control-oriented. They are the “policemen” from head office.

But…

Within this type of treasury, there is a specialist or specialists who are externally-oriented. This could be a Treasury Accountant providing other finance functions with treasury-specific information; a Projects Manager coordinating and supporting change; a Corporate Finance specialist supporting mergers, acquisitions, and customer financing. There are many types of specialists, and it’s not important for non-Treasurers to understand all types, or what they do. What’s important it they all share one thing in common: they serve as the link between Treasury and non-Treasury stakeholders. Management has made an investment into people whose main job is to deal with… other people.

This makes a big difference. Appointing specialists with an external orientation means these individuals and the treasurer can’t stay in the safe zones of technical treasury and banking. They must be proactive, communicate effectively with different people and functions, influence those they don’t control, fit in with others’ timeframes, and be flexible enough to say ‘yes, you can’ even when the main objective of treasury is still to control and say ‘no, you’re not allowed’.

Despite this increased flexibility, the fact that these specialists are a small number of people within the overall functions means these treasuries can’t fully deliver on their potential. They are “unhappy” because they can’t deliver strategically material benefits.

Stakeholder-oriented treasuries tend to evolve from control-oriented ones. Management’s intention is for them to become more strategic, but they lack the right mix of skilled human and other resources.

Value-Adding Internal-Oriented Treasuries

Value-Adding Internal-Oriented Treasuries are like Value-Adding External-Oriented Treasuries but they are not profit centres. They are breakeven centres, a concept good in theory but not realistic or desirable in practice.

Value-Adding Internal-Oriented Treasuries are like Value-Adding External-Oriented Treasuries: they are external- and results-oriented, delivering valuable services to others within the organization.

Here’s the “But” again…

These functions are not tasked with making profits. This is the stage at which you find “breakeven” or “profit-breakeven” treasuries. They are tasked with covering their costs, no more.

Like the stakeholder-oriented treasuries, value-adding internal-oriented treasuries will have specialists whose job is to support other company functions. The main difference between the two types of tactical treasuries is that value-adding internal-oriented ones explicitly charge for each service provided. They earn income from the rest of the organisation based on the specific financial products and services they provide.

It might sound strange, but running a profit centre is simpler compared to this. In a profit centre, you aim to maximize income and minimise expenses. Running a breakeven centre, on the other hand, sounds good in theory but is not realistic in practice. Targets are set at the beginning of the year but no one knows when exactly the core business will want to transact, when cashflows will happen, or how much market rates will have changed by then. These all have to be estimates, but the target is a specific zero profit. If the treasury makes too much profit, it’s “obviously” charging the core business too much; too little, and it’s “obviously” not performing well enough.

These treasuries tend to be found when there is a core-business need to offer complex and finely-priced financial products and services to customers or suppliers, but the company is risk-averse to non-core risks. Getting the best pricing but not taking on risk is a circle that can’t be squared.

“Each unhappy family is unhappy in its own way.”

Unstable but long-lasting

Faced with contradictory objectives, tactical treasuries are less effective than their strategic counterparts. Their non-Treasury stakeholders are demanding and frequently dissatisfied. The CFO changes the goalposts frequently.

But despite this, these types of treasuries are long-lasting. There are many of them. They don’t evolve. They mostly don’t cross the chasm. We’ll explain why in the next articles.

Next article: Crossing the Chasm

Previous articles in the Treasury for Non-Treasurers series:

Join our Treasury Community

Treasury Masterminds is a community of professionals working in treasury management or those interested in learning more about various topics related to treasury management, including cash management, foreign exchange management, and payments. To register and connect with Treasury professionals, click [HERE] or fill out the form below to get more information.