Cash Flow Hedging in Eruptive Currency Markets

This article is written by GPS Capital Markets This summer my family visited Yellowstone National Park. At Mammoth Hot Springs Historic District, near the north entrance of Yellowstone, I learned about the park’s history. This was the first national park ever established, with a vast coverage area (3,472 square miles or 8,992 kilometers), limited financial…

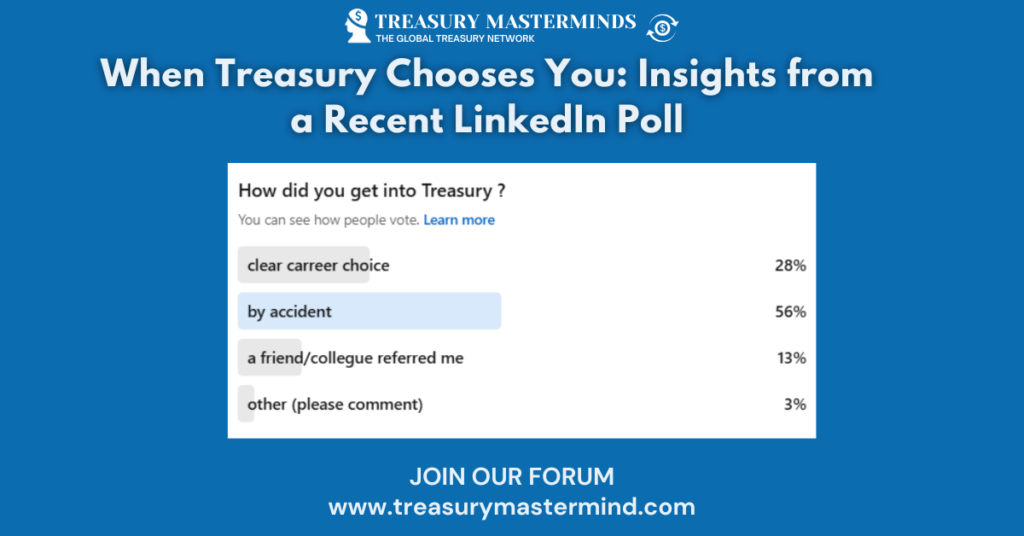

When Treasury Chooses You: Insights from a Recent LinkedIn Poll

Careers can take unexpected turns, and for many Treasury professionals, the path into their field seems to have been anything but straightforward. A recent LinkedIn poll posed the question, “How did you get into Treasury?” and the results offer a glimpse into the varied ways professionals land in this critical area of corporate finance. Here’s…

Top features to look for in in-house bank software

This article is written by Nomentia Executive summary: For global businesses looking to harmonize their cash management and gain control and visibility over their payment operations, an in-house bank is an obvious choice. In this article, we answer the following questions: What are the core functionalities of in-house bank software, and how does in-house bank…

How to Tackle Troublesome Tariffs with 5 Savvy Working Capital Solutions

This article is a contribution from our content partner, Kyriba Widespread uncertainties surround the economic impacts of the second Trump administration, especially in regards to the potential for significant tariffs on the U.S.’s top three trading partners–Mexico, Canada, and China–as well as Europe. In response to Trump’s threat of 25% tariffs on goods, both Canada and Mexico have suggested imposing retaliatory tariffs on…

Treasury Contrarian View: Treasury Dashboards — Are We Tracking the Wrong Metrics?

Dashboards have become a staple in corporate treasury—colorful visuals, real-time updates, and dozens of KPIs all packed into a single screen. But here’s the question: Are treasury dashboards helping us make better decisions, or are they just digital wallpaper? Are we tracking the right things, or are we so focused on reporting that we’re missing…

How Embedded Finance is Changing Bank Reconciliation

This article is written by Embat Embedded finance is revolutionising the way businesses and banks interact with each other, as well as with consumers and users. Advances in new technologies and the support of APIs have completely changed the current financial paradigm, altering many of the business processes we encounter daily. But how exactly is…

CBDC vs Stable Coin for Treasurers

The rise of Central Bank Digital Currencies (CBDCs) and stablecoins is a hot topic in the world of treasury and payments, particularly with the push toward faster, more efficient international transactions. Here’s a comparison of CBDCs and stablecoins, focusing on control and their potential usefulness for corporate treasurers: 1. CBDCs (Central Bank Digital Currencies) CBDCs…

Are You Checking Your FX Trade Time-stamps?

This article is a contribution from our content partner, Just The UK Financial Conduct Authority (FCA) has released a statement confirming its recognition of the updated FX Global Code. As part of that statement, the FCA also clarified its view that it is not consistent with the principles in the Code for FX providers to delay a client’s…

Dynamic Discounting

This article is a contribution from our content partner, PrimeTrade Dynamic discounting is a form of supplier finance – often grouped with supply chain finance, SCF, and reverse factoring. These are arrangements that help suppliers to get cash early when buyers do not want to pay invoices immediately. Dynamic discounting is different though Supply chain…